The federal estate tax exemption remains at an all-time high. For some families, that is genuinely good news. But it may also be creating a false sense of security, especially if you live in one of the states that sets its own rules or if your estate strategy was written before the law changed.

When the One Big Beautiful Bill Act (OBBBA) was signed into law on July 4, 2025, it set the federal estate and gift tax exemption at $15 million per person and $30 million for a married couple, with annual inflation adjustments thereafter. The sunset that estate professionals had been bracing for since these exemption amounts were increased in 2017 never arrived. For most families, this was good news.1

But here is what that headline tends to obscure: the federal number is not the only number that matters. For some families, particularly those in certain states, those who own property in multiple states, or those whose estate strategies were written years ago, the law change is precisely the reason to pull your estate documents and take another look with your loved ones and your team of professionals.

Summer is a practical time to do this. Families often come together. The year-end rush has not started. And there is no more useful conversation to have over a few unhurried days than the one that answers: Does what we have in place still reflect what we want to happen after we are gone?

The Federal Number Most Families Will Never Reach

The federal estate tax exemption of $15 million per individual means that only estates exceeding that threshold owe federal estate tax at death. For married couples, the combined threshold is $30 million. Estimates are that fewer than 0.1 percent of estates that filed returns in recent years owed any federal estate tax.2

So, if you read the headlines after the OBBBA was passed last year and assumed your estate was fine, you may be right. But we’ve identified three scenarios where a closer look is worth the time, regardless of whether your estate is anywhere near the federal threshold.

Scenario One: Your State Has Its Own Estate Tax

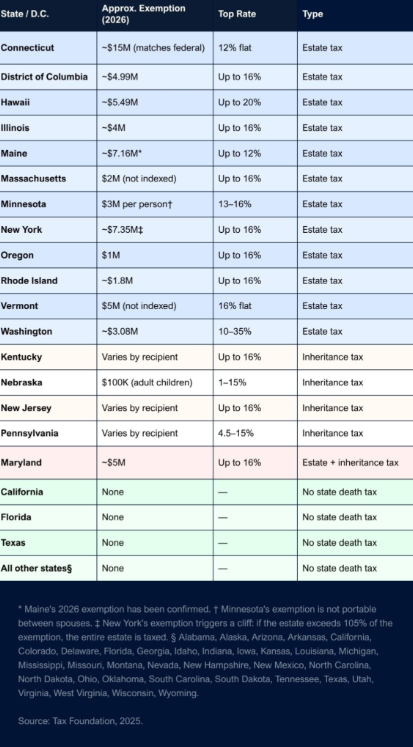

The OBBBA changed the federal exemption. It did not change a single state’s rules. Twelve states and the District of Columbia still impose their own estate taxes, and in most cases, their exemptions are lower than the federal level.3,4

Oregon and Massachusetts set their thresholds at $1 million and $2 million, respectively. In Massachusetts, that number is not indexed for inflation, meaning it has quietly been shrinking in real terms for years. A family with a paid-off home, a retirement account, and other assets might cross that line without thinking of themselves as wealthy at all.

New York has its own wrinkle, known as the “estate tax cliff.” Once an estate exceeds 105 percent of New York’s exemption (currently around $7.35 million), the entire estate is taxed, not just the amount above the threshold. A married couple in New York with a combined estate just above that line could owe New York estate taxes of several hundred thousand dollars, even though they owe nothing federally.

Five states impose an inheritance tax, with Maryland being the only one to impose both. An inheritance tax is paid by the person receiving the assets, not the estate. The rates and exemptions vary by the recipient’s relationship to the deceased and can impact more than just the wealthy.

Before looking at the state-by-state picture, it helps to understand the difference between the two types of taxes that can apply at death. They are often used interchangeably, but they work very differently and affect different people.

It’s important to point out that this blog is laying out some high-level issues regarding estate taxes and how they might apply in certain states. We would encourage you to speak with an estate professional, who can address your specific situation.

Estate Tax vs. Inheritance Tax: What’s the Difference?

The estate itself pays an estate tax before assets are distributed to heirs. It is calculated based on the total value of everything the deceased owned at death, including real estate, retirement and investment accounts, life insurance proceeds if the deceased owned the policy, business interests, and personal property. If the estate’s total value exceeds the applicable exemption, the estate pays the tax before anything is passed on. The heirs receive whatever remains after the tax is settled. At the federal level, and in most states that impose one, the estate’s executor or administrator handles this obligation.

An inheritance tax works differently. It is paid by the person receiving the assets, not by the estate. The amount owed depends not on the total size of the estate but on the value of what each individual heir receives and how closely related they are to the deceased. Close relatives, typically spouses and children, are usually exempt or taxed at lower rates. More distant relatives or unrelated heirs often face higher rates with much smaller exemptions. In Nebraska, for example, adult children owe inheritance tax on amounts above $100,000. In Kentucky, nieces and nephews receive only a $1,000 exemption before the tax kicks in. The heir pays this out of their own inheritance, not out of the estate.

The practical difference matters in preparing a strategy. With an estate tax, the question is whether the estate’s total value clears the exemption threshold. With an inheritance tax, the question is who is receiving assets and how much each person gets. A family could have an estate well below any estate tax threshold and still face an inheritance tax bill if assets pass to non-immediate family members, such as a niece, a close friend, a domestic partner in certain states, or a sibling, depending on the state involved.

Maryland is the only state that currently imposes both. Qualifying estates there may owe state estate tax on the total value of the estate, and individual heirs may separately owe inheritance tax on what they receive. Spouses are generally exempt from inheritance tax in every state that imposes it, but the rules for other relatives vary enough that it is worth knowing your state’s specific treatment.

The table below shows which states currently impose estate or inheritance taxes, along with approximate 2026 exemptions and top rates.

Where Does Your State Stand on Estate and Inheritance Taxes?

Scenario Two: You Own Property in More than One State

Estate and inheritance taxes follow property, not just people. If you own a vacation home, investment property, or any real estate in a state other than where you live, your estate may be subject to that state’s rules even if your home state has no death tax of its own.

For example, a Florida resident with a vacation home in Vermont would owe no Florida estate tax (because there isn’t one). Still, Vermont’s $5 million exemption and 16 percent flat rate would apply to the Vermont property. Someone who lives in Texas but inherited a rental property in Oregon could face Oregon’s $1 million threshold on that asset.

This is one of the least-discussed dimensions of estate preparation and one of the most common sources of surprise for families who assumed their strategy covered everything. If any real or tangible property sits in a different state than where you live, it is worth confirming how that state’s rules apply to your situation.

Scenario Three: Your Documents Were Written for a Different Law

Even if your state has no estate tax and your estate is well below the federal threshold, there are other reasons an estate strategy may no longer reflect what you actually want or what the law now allows.

Many strategies were designed around the anticipated expiration of the higher exemption. Credit shelter trusts, bypass trusts, and certain irrevocable structures were built to capture a lower exemption before it disappeared. Now that the exemption has increased rather than decreased, some of those structures may be doing nothing useful or creating unintended consequences.

One specific issue worth understanding is that assets held in a bypass trust or credit shelter trust typically do not receive a step-up in cost basis at the surviving spouse’s death.5

That means heirs who eventually sell those assets may owe capital gains taxes on decades of appreciation that they may have avoided entirely had the assets passed through the estate. In a world where estate taxes are no longer a concern for most families, holding appreciating assets in a trust that blocks the step-up can be a significant and often unnecessary cost.

Setting up a trust involves navigating complex tax rules and regulations. If you have a credit shelter trust, bypass trust, or another type of trust, you might want to have the document reviewed by a legal professional who can help determine if changes might be needed.

Beyond trust structures, several other elements of an estate strategy deserve a fresh look regardless of the tax landscape:

- Beneficiary designations on retirement accounts and life insurance policies typically override everything in a will or trust. They are also among the most commonly outdated documents when it comes to an estate. Courts have upheld transfers to ex-spouses, deceased relatives, and unintended heirs because designations were never updated after a life change.

- Powers of attorney and healthcare directives should reflect your current wishes and name people who are still living, still capable, and still the right choice. If you haven’t reviewed these documents in a while, you may be surprised by who you named in the past.

- Executors and trustees named years ago may have since moved, declined in health, or changed their relationship with your family. An executor who is 20 years older than you may have made sense at the time, but may not be the right person to manage a complex estate today or in the future.

- Asset titling (how property is legally owned) determines what passes through probate and what does not. A trust that holds no assets because titling was never updated is effectively a very expensive piece of paper.

There is no deadline attached to this. The law is not expiring. The urgency here is not tax-driven; it is life-driven.

Estate strategies can go out of date in two ways. It can happen slowly, as the law changes around them, or suddenly, when a family member dies, divorces, remarries, or has children. Some families update their documents after sudden events and don’t consider the impact of the slow drift. The result may be a document that was carefully prepared at one point in time but has not kept pace with either the family or the law since.

Summer vacations are often a time when families are together. A weekend together is when the older generation and the adult children finally have an unhurried conversation about what is in place, who has the documents, and whether it still makes sense. Conversations surrounding mortality may be difficult to talk about, but they are necessary, and putting them off because they might be difficult isn’t doing anyone any good. That conversation does not have to start around a conference table in a professional’s office. It can begin more informally with a question like, “When did we last look at this?”

But after the subject is broached, we, as financial professionals, can help facilitate exactly the kind of review that gives your family real clarity. We recommend a working session to review estate documents, check beneficiary designations, and identify what needs a second look from an estate attorney. For many families, that review has never happened in a coordinated way. This summer is a great time to do it. If you or someone you know would benefit from this, we’d welcome the opportunity.

Frequently Asked Questions

Do I Need an Estate Strategy if My Estate Is Well Under $15 Million?

Yes, for reasons unrelated to the federal estate tax. An estate strategy is the legal framework that determines who receives your assets, who manages your affairs if you cannot, and who makes medical decisions on your behalf. Beneficiary designations, powers of attorney, healthcare directives, and asset titling all matter independently of your tax situation.

I Live in a State With No Estate Tax. Does This Still Apply to Me?

It may. If you own property in a state that does impose an estate or inheritance tax, such as a vacation home, investment real estate, or even land, that state’s rules may apply to those assets regardless of where you live. A strategy written five or ten years ago was built around assumptions about your family, your assets, and the law that may have shifted in ways worth addressing.

My Parents Have a Trust That Was Set Up Years Ago. Does It Need to Be Updated?

Many trusts created before 2025 were built around certain expectations about the federal estate tax exemption. It is worth having an estate attorney review the specific language to determine whether the structure still serves the family’s goals.5

What Does a Financial Professional Do in an Estate Strategy Review?

A financial professional typically plays a coordinating role rather than drafting legal documents, which remains the domain of an estate attorney. In a review, a financial professional can help gather and organize the existing strategy, check that retirement accounts and other documents carry the correct beneficiary designations, confirm that assets are titled consistently with your intent, identify anything that may have been overtaken by life events or legal changes, and flag the specific issues that warrant a conversation with an attorney. As financial professionals, we often refer to ourselves as our clients’ quarterbacks, helping their professional team, including lawyers, accountants, business consultants, and others, is following the same playbook.

Sources:

1. Forbes, July 3, 2025

https://www.forbes.com/sites/matthewerskine/2025/07/03/estate-planning-and-the-final-obbba-key-changes-high-net-worth-individuals-must-know/

2. Center on Budget and Policy Priorities, December 19, 2025

https://www.cbpp.org/research/federal-tax/the-federal-estate-tax

3. Tax Foundation, October 28, 2025

https://taxfoundation.org/data/all/state/estate-inheritance-taxes/

4. AARP, March 31, 2026

https://www.aarp.org/money/retirement/states-with-estate-inheritance-taxes/?msockid=37914d74d918692c38995a5cd8f4687f

5. Commerce Trust, August 30, 2024

https://www.commercetrustcompany.com/research-and-insights/articles/understanding-credit-shelter-trusts-versus-portability

Disclosure: This blog is for informational and educational purposes only and does not constitute legal or tax advice. Estate planning rules vary significantly by state and individual circumstance. Consult a qualified estate planning attorney and financial advisor before making decisions based on this content. State exemption amounts and rates are subject to change.