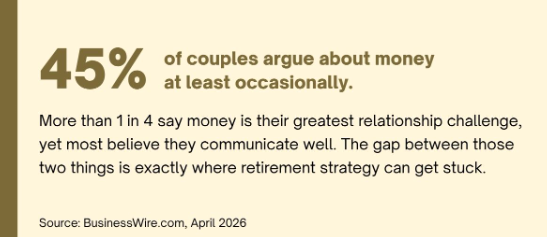

As financial professionals, we spend much of our time helping our clients prepare for retirement. By the time most of our clients are within a few years of retirement, their savings are there, their investment accounts are in order, and their income strategy is in place. From a financial standpoint, everything looks good on paper. That’s when we ask them a more difficult and personal question: Have you two actually talked about what retirement will be like? Not the math. Your life. Where you’ll be, how you’ll spend your time, and what each of you is genuinely looking forward to. We find that many have not thought that far ahead.

The data backs this up in some uncomfortable ways. Fidelity’s 2024 Couples and Money Study, which tested 1,794 couples by surveying each partner separately, found that 53 percent of couples who have not yet retired hold conflicting views on how much they need to save, and only 57 percent rate their household’s financial health as excellent or very good.1

These are not small gaps. They are the kinds of misalignments that potentially can upend a retirement strategy.

The Timing Problem Not Talked About Until It’s Too Late

More than two-thirds of working couples expect to retire at the same time or within a year of each other, according to Ameriprise Financial’s 2024 Couples, Money, and Retirement study.2

It’s a common assumption couples make and one that rarely comes true.

The gap between expectation and reality here is not just a scheduling inconvenience. When one partner retires, and the other does not, the household dynamic changes in ways many couples are not prepared for. The retired partner may lose some professional identity and daily structure. The still-working partner may come home to a different kind of pressure. Who manages the house? Who handles the money? What does the retired partner do with eleven hours of unstructured time?

None of these questions is unanswerable. But they can be much easier to answer before one person has already retired than after. A staggered retirement, done intentionally and with a clear purpose, can actually be a smart financial strategy. The working partner can keep building savings, delay Social Security, and maintain health coverage. Done by surprise, the same situation may create friction that is hard to unwind.

A valuable thing couples can do in the five years before either of them retires is to talk specifically about this scenario: what happens if we do not retire at the same time, and what does each of us need and expect if that is the case?

Questions Worth Asking Before You Retire

Several important questions can reveal potential misalignments in retirement expectations. Here are six that you and your partner may have been sidestepping but need to ask each other as you near retirement.

Where Will We Live, and Have We Both Truly Agreed?

This is the conversation with perhaps the largest financial consequences and the longest lead time needed to address. One partner may have been spending the last decade looking forward to living in a warmer state. The other may have assumed they were staying in the house where they raised their family. Both have made this assumption in good faith and maybe in silence. Cost of living, proximity to children and grandchildren, access to medical care, and what to do with the primary residence all depend on this one question having a real answer, not an assumed one.

How Will We Build Meaningful Structure in Retirement?

Retirement removes the structure that most people have used to organize their lives. For some people, that’s a relief. For others, it’s destabilizing in ways they did not anticipate. The couples who tend to navigate this change most smoothly are those who have already thought about what will replace work, not just financially but personally. Board service, consulting, a creative practice, a physical commitment, or a volunteer role. These are not hobbies. They’re sources of identity—and worth thinking through together, especially in your early retirement years.

This may also matter for your relationship. Couples who suddenly spend every hour together after decades of parallel busy lives sometimes discover they need more intentional structure around both togetherness and individual space than they expected.

Retirement means a lot more time together—and while that’s wonderful, it can also be an adjustment. Talking openly about how you’d each like to spend your days can go a long way.

How Will We Handle Healthcare, and Do We Understand What It Will Actually Cost?

A 65-year-old retiring in 2025 can expect to spend approximately $172,500 on healthcare over the course of their retirement, according to Fidelity’s 2025 Retiree Health Care Cost Estimate. For a couple, that figure climbs to roughly $345,000.3 These estimates assume enrollment in Medicare and do not include long-term care.

What surprises most couples is not the healthcare number itself but the complexity of getting there. Medicare decisions are not simple. The income-related monthly adjustment amount (IRMAA) surcharges increase Medicare Part B and Part D premiums for certain high-income enrollees. In 2026, the surcharge applies to people with a modified adjusted gross income above $109,000 (individual return) or $218,000 (joint return).4

Couples with an age gap may face a Medicare coverage gap if one partner retires before 65. And every choice involves trade-offs among premium cost, provider access, and out-of-pocket exposure, which differ across partners. A Medicare professional might offer some guidance.

What If One of Us Needs Significant Extended Care?

According to the U.S. Department of Health and Human Services, 56 percent of adults turning 65 between 2021 and 2025 are expected to need some form of long-term services and support during their lifetime.5

A couple facing extended care expenses sees their wealth decrease by an average of 21 percent over nine years, according to Morningstar research. The decisions available at 70 can be more expensive and more limited than those available at 58 or 62.6

Most couples put this conversation off, not because they do not care about the answer, but because confronting the possibility of illness can be uncomfortable. That discomfort is worth pushing through early.

The question to answer together is not “Which facility would we prefer?” It is, “What is our financial strategy if this happens, and have we done anything to prepare?”

How Will We Coordinate Social Security, and Have We Considered Both Partners’ Situations?

A Social Security claiming strategy is one of the highest-value decisions a couple makes. The timing of one partner’s claim affects the survivor benefit available to the other. Delaying benefits may increase the surviving partner’s lifetime income. On the other hand, claiming early to fund current expenses may lower the investment drawdown math for the years before both partners are collecting.

While you can start claiming Social Security benefits as early as 62, doing so reduces your monthly benefit. Delaying until age 70 increases your benefit to your maximum level.

Here are the maximum monthly benefits at various ages for someone who earned at or above the taxable maximum during their career:

It’s not about finding the “best age” to claim, but rather identifying the age that best fits a couple’s personal situations and goals. There is no universally right answer. But the answer should come from a review of both partners’ earnings records, health trajectories, and income needs, not from an assumption.

When talking with your partner about claiming Social Security, consider treating it like a strategic project, not just an election on a government form. While Social Security may not be your primary source of retirement income, it can still play a significant role in a comprehensive retirement strategy.

Do We Have a Financial Strategy?

Despite the stakes involved, having a formal strategy remains the exception rather than the rule for some. Among couples with at least $100,000 in investable assets and within ten years of retirement, Ameriprise’s 2024 research found:

These are couples who have simply not yet had a conversation about their retirement strategy. The delay is not necessarily avoidance in the negative sense. It may be the same thing that prevents the most important conversations from happening: no one has created the structure or the occasion for it. But you and your partner can change that. A trusted financial professional can help you identify some challenges and help you address the gaps in preparation.

What It Looks Like When Couples Talk About Retirement With a Professional

The conversation that happens in a meeting with a financial professional tends to look different from the version couples attempt on their own at the kitchen table. Part of it is having an agenda that gives permission to raise things that might otherwise feel too big or too uncomfortable to introduce.

What we consistently find is that most couples are not as far apart as they might think. The partner who wanted the beach house has usually also been thinking about the grandchildren. The partner who wanted to stay put has been wondering about weathering the winters as they get older. The differences are real, but they are negotiable in ways that rarely feel so when they sit unspoken.

The couples who get the most out of these conversations are the ones who come in willing to be surprised by what their partner actually thinks, rather than defending the version of the conversation they imagined having. That willingness, more than any financial variable, tends to predict how well retirement goes.

If you and your partner have been putting off this conversation, summer is a genuinely good time for it. The pace is different. There is room to think. And the conversations that feel large in the abstract tend to become much more manageable once they start.

Questions We Hear Often

What Should Couples Talk About Before One of Them Retires?

Some of the most important conversations center around where you will live, when each of you will stop working, your extended care strategy, how you will coordinate Social Security, and what each of you individually needs from your days to feel purposeful. Of these, the last one tends to have the most impact on relationship satisfaction in retirement and gets the least attention in financial conversations.

Is It Normal for Couples to Disagree About Retirement?

Ameriprise’s 2024 research found that 25 percent of couples disagree on what they’ll spend on travel and experiences, and 24 percent disagree on financial support for children and grandchildren.7

None of these disagreements is unusual, and most are resolvable when brought up in a structured conversation rather than left to simmer.

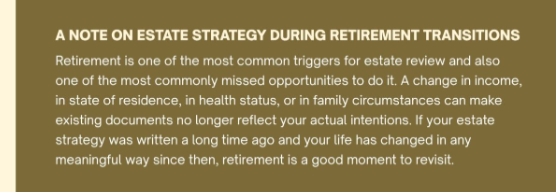

How Do We Know if Our Estate Strategy Is Still Current?

If your estate strategy was written before your most recent change in residence, health status, family structure, or asset picture, it should be reviewed. The documents to review include your will, durable power of attorney, healthcare directive, beneficiary designations on all accounts, and any legal structures in place.

What Should We Know About Healthcare Costs Before We Retire?

Fidelity’s 2025 Retiree Health Care Cost Estimate projects $172,500 per person and approximately $345,000 per couple for healthcare expenses over the course of retirement. This covers Medicare premiums and out-of-pocket costs but not extended care. The figure has risen more than 4 percent year over year and has more than doubled since Fidelity began tracking it in 2002.3

The most important insight is that Medicare is not the whole answer. It is not comprehensive and requires more complex decision-making than most people realize. Those decisions can benefit from being discussed in advance, not right before the enrollment deadline.

The Time to Start Having Real Retirement Conversations Is Now

By taking the time now to discuss a well-thought-out retirement strategy, you can set yourself and your partner up for success at a time of life you should both enjoy. As financial professionals, we help our clients work through the many aspects of retirement. We can also help facilitate discussions that are often more difficult about what retirement will really look and feel like. If you’re ready to talk, we’re here to help.

Sources:

- BusinessWire.com, April 2026

https://www.businesswire.com/news/home/20240201922762/en/Love-Money-Most-Couples-Give-Themselves-High-Marks-in-Communication-Yet-Fidelity-Study-Reveals-Hidden-Frustrations-in-Couples-Financial-Future - Ameriprise.com, April 2026

https://www.ameriprise.com/binaries/content/assets/ampcom/amp_research-report.pdf - NewsRoom.Fidelity.com, July 30, 2025

https://newsroom.fidelity.com/pressreleases/fidelity-investments–releases-2025-retiree-health-care-cost-estimate–a-timely-reminder-for-all-gen/s/3c62e988-12e2-4dc8-afb4-f44b06c6d52e - NerdWallet.com, January 15, 2026

https://www.nerdwallet.com/insurance/medicare/learn/what-is-the-medicare-irmaa?msockid=37a2e58496ac672b39a4f4af9742667d - AARP.org, March 12, 2026

https://www.aarp.org/caregiving/financial-legal/long-term-care-affordability-report/ - CFSWV.com, January 2, 2024

https://cfswv.com/cfsblog/long-term-care-statistics-to-know-for-2024 - Financial-Planning.com, April 19, 2024

https://www.financial-planning.com/news/quarter-of-couples-disagree-over-retirement-spending-priorities